Intel shines amidst the carnage of the 2019 semiconductor market

It was a year when global semiconductor revenue fell by the greatest percentage in at least two decades, when eight of the top-10 chip suppliers suffered revenue declines and when sales fell for every application market and for every global region. The year 2019 was also the time when Intel bucked the trend—achieving growth and reclaiming the market’s top spot as the company’s long-term diversification strategy paid dividends during a challenging period for the semiconductor business, according to Omdia.

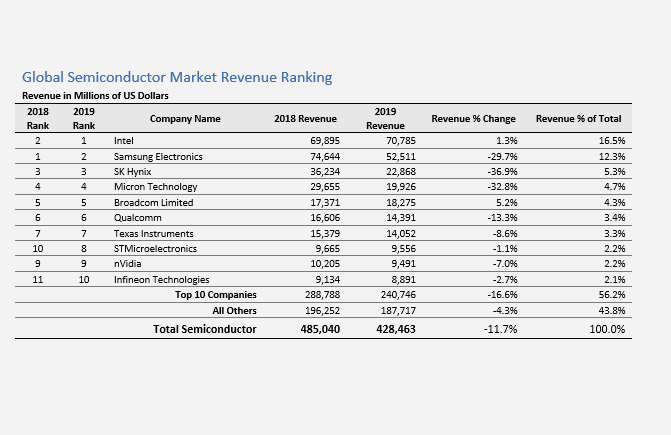

Global semiconductor revenue plunged by 11.7 percent in 2019, shedding $56.6 billion worth of revenue compared to 2018. This represented the worst annual performance for the chip industry since Omdia began gathering data in 2001—and the most notable drop since 2009, when revenue fell by 10.9 percent, as reported by the Omdia Competitive Landscaping Tool.

Top semiconductor suppliers that are heavily dependent on the memory segment bore the brunt of the market plunge, with Samsung Electronics, SK Hynix and Micron Technology all posting revenue declines in about the 30 percent range.

In contrast, Intel managed to attain 1.3 percent growth, allowing the company to rise one position in the ranking and surpass Samsung as the world’s top semiconductor supplier in 2019. For Intel, this growth represents the payoff for a diversification strategy that’s five years in the making.

“Intel’s performance in 2019 represents a triumph for the company’s diversified business model,” said Ron Ellwanger, senior analyst, semiconductor manufacturing, for Omdia. “Five years ago, Intel began to refocus its business strategy into various critical products and end markets. This strategy has paid off in 2019, allowing Intel to avoid dependence on a single product or application market and enabling the company to mitigate the effects of the massive market downturn of 2019.”

Significantly, Intel achieved zero growth in its core microprocessor business in 2019, illustrating the company’s success in other segments. For example, sales of logic chips rose 7.1 percent.

Inside Intel’s business structure

Intel currently has five groups covering the following segments: data center, internet of things (IoT) including autonomous driving, 3D NAND flash memory for solid-state drives, programmable semiconductors and PCs. Four out of five of these groups attained growth and posted record-high revenue in 2019—a major accomplishment in a year of a double-digit market decline.

Intel’s Mobileye division focused on autonomous driving achieved the most impressive growth, with revenue rising by 25.9 percent for the year.

However, the larger Data Center Group (DCG) and Internet of Things Group (IOTG) were the real drivers of the company’s revenue expansion for the year. DCG, which accounts for 33 percent of company revenue, attained 2.1 percent revenue growth in 2019. IOTG, which represents 5 percent of Intel sales, grew by an impressive 10.6 percent for the year.

Intel finds gold in the struggling data-center segment

The DCG performance is all the more remarkable given that global semiconductor market revenue for data-center applications fell by gut-wrenching 16.2 percent for the year—the largest decrease in more than a decade. Overall, the data-center segment suffered from slowing demand, as customers burned through inventory during the first two quarters of the year, rather than purchasing new chips.

Despite the horrendous industry conditions, Intel was able to go to market with data-center oriented products that commanded higher average selling prices (ASPs). The increase in ASPs enabled Intel to overcome the impact of reduced unit sales, allowing the company to attain impressive growth in the segment.

“Once regarded as PC-centric microprocessor supplier, Intel is now a diversified vendor of solutions ranging from logic chips, to software, to analytics,” Ellwanger said. “Omdia believes that Intel’s diversification strategy will continue to serve the company well—in good times and bad. While commodity sectors like memory will always be riding the ups and downs of the boom-and-bust cycle, Intel has built its foundation on attractive semiconductor market segments and value-added products that can deliver sustained growth.”

Sony’s sensor salvation

Another standout performer in 2019 was 13th-ranked Sony Semiconductor Solutions Corp., which attained stunning growth of 30.9 percent for the year. The massive increase in revenue allowed the company to rise four places from the 17th rank in 2018.

“Sony’s performance was built on its leadership position in CMOS image sensor chips, which are used as cameras in a wide variety of devices—including smartphones,” Ellwanger said. “With smartphones increasingly employing multi-camera configurations, demand for Sony’s consumer-quality sensors is soaring.”

Triple-camera smartphones became the most popular type of model on the market in the fourth quarter, exceeding dual-camera devices for the first time, according to Omdia. Models with three cameras accounted for 31 percent of global smartphone shipments during the final three months of 2019, exceeding the percentage of single-camera models. This helped drive a 22.9 percent increase for the global CMOS sensor market in 2019.

Highlights from a year of lows

Other major development arising from 2019 include:

• Memory chip revenue plunged by 31.6 percent, with DRAM falling 37.2 percent and NAND flash memory dropping by 24.5 percent—despite a stabilization in pricing in the fourth quarter.

• The wireless communications segment cratered by 13.3 percent for the year—the largest decline in more than 10 years. Mobile sales declined for the year as consumers delayed phone purchases while waiting for true 5G performance.

• Artificial-intelligence chipmaker suffered a 7 percent revenue decline for the year, again the largest decrease in more than a decade.