Elpida Bankruptcy Aids The Semiconductor DRAM Market

IHS says that partly following the exit of major manufacturer Elpida Memory Inc., the global DRAM industry revenue this year is forecast to reach $30.6 billion, up 3.3 percent from $29.6 billion in 2011.

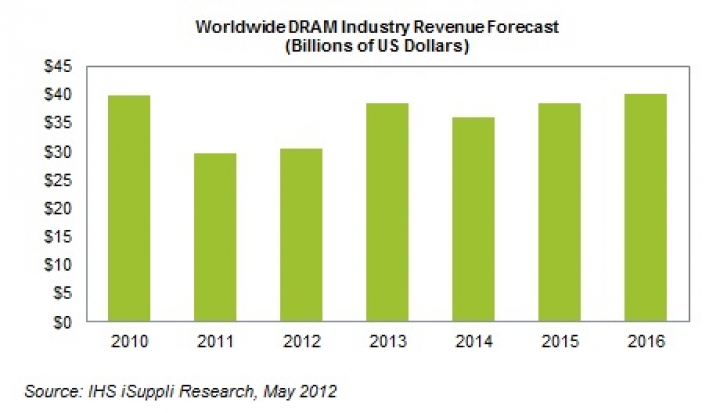

This may sound like a small amount but the revenue

expansion for 2012 is a welcome development given the stunning 25 percent

contraction last year.

The overall picture is expected to brighten during the next few years, as shown in the figure above, with DRAM revenue exceeding $30 billion each year for the next five years and reaching $40.2 billion in 2016. This is an unprecedented new high for the market.

"This year's anticipated turnaround comes as somewhat of a surprise, especially as the challenges of 2011 appeared to point to a calamitous 2012," says Mike Howard, senior principal analyst for DRAM & memory research at IHS. "Weak demand was one of the major challenges last year, when revenue slipped each quarter as prices went from bad to worse. However, the key problem was excess DRAM manufacturing capacity, the same trouble that has bedevilled the industry for much of its history."

The Thailand floods in October last year depressed PC shipments, a traditional DRAM stronghold. The perceived scarcity of hard disk drives caused PC sales to plummet affecting DRAM demand; and the paucity of hard drives meant PC manufacturers were paying more for storage, leaving even fewer dollars to spend on DRAM.

DRAM prospects started looking better, however, after the bankruptcy filing in February of Japan's Elpida. Elpida was part of the elite echelon of DRAM manufacturers that includes Samsung Electronics Co. Ltd. and Hynix Semiconductor Inc. of South Korea, as well as U.S.-based Micron Technology Inc.

"Elpida's insolvency will have a massive impact on the industry's fortunes, primarily because it promises to shift the market from a state of endemic oversupply to sorely needed balance for most of 2012," Howard notes. "As a result of such developments, IHS is now cautiously optimistic that the DRAM industry may actually be through the downturn and headed for improvement."

Even with the final outcome of Elpida's bankruptcy uncertain and the disposition of its assets still in negotiation, the rest of the industry is expected to benefit from Elpida's exit, with the market lifting on signs of supply rebalance.

What's more, no significant deterioration is expected within the global economic environment, which should help reverse the paucity of demand that has hobbled the industry of late.

The DRAM space can look forward to continued strong expansion in the next few years because of three powerful growth drivers: ultrathin PCs, smartphones and tablets.

Ultrathin PCs, a category that includes Intel's

ultrabooks, the MacBook Air from Apple and ARM-based lightweight PCs"”will

present plenty of new opportunities for low-power DRAM, especially when

ultrathins comprise the majority of shipments by 2016.

For high-end ultrabooks in particular, PC manufacturers are projected to have enough margin to afford the installation of low-power double data rate 3 (LPDDR3) DRAM in their products, adding to overall DRAM industry revenue. LPDDR3 will account for as much as 19 percent of the total DRAM market in 2014.

In the case of smartphones, increasing shipments during the next five years coupled with growing memory content per phone suggest rosy prospects as well for DRAM. Average DRAM content in smartphones this year will amount to 5.1 gigabits, up from 3.5 gigabits last year and from 2.3 gigabits in 2010.

Overall, the net increase in DRAM due to smartphones will equate to a compound annual growth rate (CAGR) of 65 percent from 2011 to 2016.

Very rapid growth is also forecast for DRAM in tablets, with average DRAM content in 2012 for the devices projected to hit 8.0 gigabits, up from 4.5 gigabits last year and 2.5 gigabits in 2010. When tablet shipment increases are combined with DRAM content growth, DRAM use in tablets will be up a substantial 95 percent CAGR for the same five-year period from 2011 to 2016, accompanying smartphones and ultrathins in boosting total DRAM revenue.