SEMI: Fab equipment spending to remain flat in 2013

When forecasting fab spending, capacity ramps, and related technology node transitions, analysts must not only examine the semiconductor industry, but also track and consider economic factors. These include GDP, political events, oil prices, unemployment rates, and consumer sentiments.

The latest SEMI World Fab Forecast report, published at the end of November 2012, reveals major changes from previous estimates for 2013.

With macro factors such as the slowing Chinese economy, turmoil in the Middle East, the United States fiscal cliff and debt ceiling debates, and the official "double dip" recession in Europe, big capital spenders have revised their current spending plans. The outcome of the election in South Korea and patent suits with Apple also may affect Samsung's capex decisions for 2013.

A Year of Uncertainty

Despite current difficult times and unknowns, growing demand for mobile devices, such as tablets and phones, inspires an improved outlook for chip sales in 2013. Various forecasts range from 4 to 16 percent, averaging 7 percent, revenue growth next year.

Typically, chip sales and capex ride the same roller coaster, as observed that in the past; however, 2013 appears to be another year of uncertainty. While chip sales may rise in 2013, some perspectives for equipment sales range from low single digit growth down to negative double digits.

The largest spenders on fab equipment are TSMC, Samsung, and Intel, yet the latter two have yet to make any official announcements about their 2013 capex plan. Using bottom-up methodology, the World Fab Forecast is able to project quarter by quarter fab equipment and fab construction spending, as well as capacity addition and expected changes in technology nodes, based on currently known information and plans.

Fab equipment spending for Front End Fabs to remain flat in 2013

In August, the World Fab Forecast report predicted 17 percent growth for Front End equipment, which was revised downward to 0 percent growth (flat) (or US$ 32.4 billion, including Discretes and LEDs, used equipment and in-house equipment) in the November report.

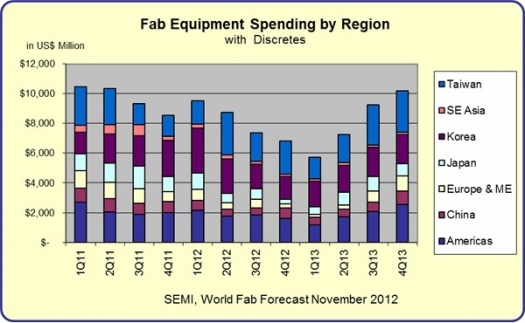

Possible scenarios for 2013 vary from -5 percent to +3 percent change for equipment spending, mainly pending capex plans by TSMC, Intel and Samsung. The projected number of facilities equipping will drop from 212 in 2012 to 182 in 2013. What's more, Fab equipment spending saw a drastic dip in 2H12 and, accounting for seasonal weakness and near-term uncertainty, 1Q13 is expected to be even lower (See figure at the top of this story).

Examining equipment spending by product type, System LSI is expected to drop in 2013. Spending for Flash declined rapidly in 2H12 (by over 40 percent) but is expected to pick up by 2H13. The foundry sector is also expected to increase in 2013, led by major player TSMC, as well as Samsung and Globalfoundries.

Construction Spending Up in 2013

While fab construction spending slowed in 2012, at -15 percent, the SEMI World Fab Forecast report projects an increase of 3.7 percent in 2013 (from $5.6 billion in 2012 to $5.8 billion in 2013). The report tracks 34 fab construction projects for 2013 (down from 51 in 2012). An additional 10 new construction projects with various probabilities may start in 2013. The largest increase for construction spending in 2013 is expected to be for dedicated foundries and Flash related facilities.

Capacity Additions Slow in 2012 and 2013

Many device manufacturers are hesitating to add capacity due to declining average selling prices and high inventories. This is pronounced in the Flash sector, as seen with Sandisk investments since the beginning of 2012 and both Samsung and Toshiba starting 3Q12.

The figure below displays World Fab Forecast data showing a sharp decline in installed capacity growth rates for 2012 and 2013 compared to 2010 and 2011 rates.

Worldwide Installed Capacity

Breaking down the industry by product type, growth of capacity for System LSI will be less robust (20 percent increase in 2012, down to 14 percent in 2013). Flash capacity additions dragged in 2H12, with a sluggish 2 percent expansion overall for the year. However, the SEMI World Fab Forecast data show more activity by mid-2013, with nearly 6 percent growth, adding over 70,000 wafers per month (in 300mm equivalents for Flash. The data also point to a rapid increase of installed capacity for new technology nodes, not only for 28nm but also from 24nm to 18nm and first ramps for 17nm to 13nm in 2013.

Potential to Improve in 2013

If the global economy and GDP begin to show improvement and higher single-digit chip sales growth proves to be right, the equipment spending growth may ride the same roller coaster again and has the potential to go even higher for 2013. Modelling some of these scenarios, SEMI expects equipment spending for Front End Fabs could be between -5 percent to +3 percent in 2013.