China and US bolster semiconductor independence

TrendForce’s latest findings reveal that as of 2023, Taiwan holds approximately 46% of global semiconductor foundry capacity, followed by China (26%), South Korea (12%), the US (6%), and Japan (2%).

However, due to government incentives and subsidies promoting local production in countries like China and the US, the semiconductor production capacities of Taiwan and South Korea are projected to decrease to 41% and 10%, respectively, by 2027.

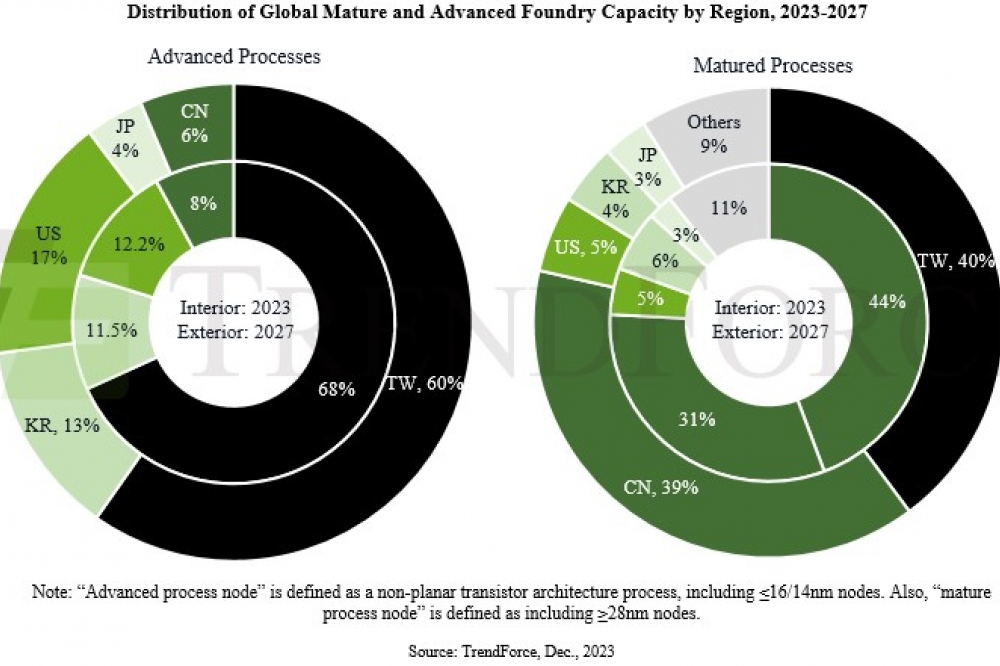

Taiwan to concentrate 60% of advanced manufacturing processes by 2027, retaining a hold on key technologies

In advanced manufacturing processes (including 16/14nm and more advanced technologies), Taiwan leads with a 68% global capacity share in 2023, followed by the US (12%), South Korea (11%), and China (8%). Meanwhile, Taiwan holds nearly 80% when it comes to EUV generation processes (such as 7nm and beyond).

In response to the concentration of semiconductor manufacturing capacity in Taiwan, the US, which has a high demand for advanced processes, is actively encouraging and supporting major companies such as TSMC, Samsung, and Intel. 2027, the US’s share of advanced process capacity is expected to increase to 17%, although TSMC and Samsung will still account for over half of this capacity.

Japan is also planning a return to semiconductor manufacturing, actively supporting local company Rapidus with a goal of reaching the most advanced 2 nm process. They aim to create a semiconductor cluster in Hokkaido and are offering subsidies to foreign companies, including Japan Advanced Semiconductor Manufacturing (JASM) and PSMC’s Sendai plant (JSMC).

China’s mature process capacity is set to grow to 39% as Taiwanese firms actively cultivate unique technological advantages

China is focusing aggressively on mature process technologies (28nm and older), particularly in response to export controls on advanced equipment by the US, Japan, and the Netherlands. By 2027, China’s share in mature process capacity is expected to reach 39%, with room for further growth if equipment procurement proceeds smoothly.

However, as Chinese manufacturers rapidly expand their mature process capacities—backed by government subsidies—this could lead to intense price competition in products like CIS, DDI, PMIC, and power discrete, impacting Taiwan-based foundries like UMC, PSMC, and Vanguard. Vanguard is expected to be most affected due to its product line including LDDI, SDDI, PMIC, and power discrete. Other companies like UMC and PSMC will maintain their advantages in the 28/22nm OLED DDI and memory sectors.

In response to chip shortages and geopolitical influences, fabless customers are diversifying risk by working with multiple foundries, potentially leading to increased IC costs and concerns over duplicate orders. Customers are also requiring global validation of production lines, even with long-term foundry partners, to enable flexible capacity adjustments. Consequently, foundries must navigate larger scale capacity and price competition while needing to maintain profitability, flexibility in capacity adjustments, new capacity depreciation pressures, and technological leadership.