Gartner: Memory spurs semiconductor revenues

In 2013, the booming DRAM market propelled strong growth for memory makers and the semiconductor industry in general

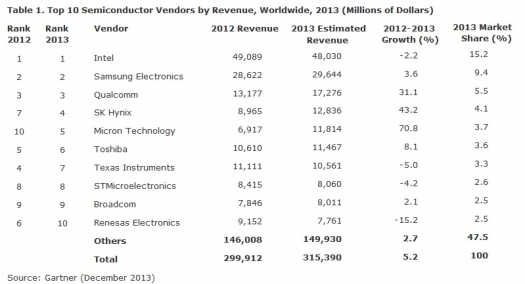

Worldwide semiconductor revenue totalled $315.4 billion in 2013, a 5.2 percent increase from 2012 revenue of $299.9 billion, according to preliminary results by Gartner, Inc.

The top twenty semiconductor vendors' combined revenue increased 6.2 percent, a significantly better performance than the rest of the market, whose revenue growth was 2.9 percent. This was, in part, due to the concentration of memory vendors, which saw significant growth in the top ranking.

"After a weak start to 2013 due to excess inventory, revenue growth strengthened in the second and third quarters before levelling off in the fourth quarter. Memory, in particular DRAM, led this growth, not due to strong demand, but rather weak supply growth," says Andrew Norwood, research vice president at Gartner.

"In fact, the overall market faced a number of demand headwinds with PC production declining 9 percent and the premium smartphone market showing signs of saturation, with growth tilting toward lower-priced, entry-level and midrange smartphone models. These demand headwinds become very visible when looking at revenue growth outside of memory, where the rest of the semiconductor market could only muster 0.4 percent growth."

Intel recorded a 2.2 percent revenue decline (as shown in Table 1 above) as strong performance in its data centre and embedded systems group was not enough to offset a declining PC market, and limited traction and declining prices for its tablet and smartphone solutions.

However, the company maintained the No. 1 market share position for the 22nd consecutive year, capturing 15.2 percent of the 2013 semiconductor market, down slightly from its peak of 16.5 percent in 2011.

As a group, memory vendors outperformed the rest of the semiconductor industry.

"Within the memory market DRAM was in the midst of a strong rebound following two years of revenue decline; the recovery started at the end of 2012 when the market was moving back into an undersupply due to lack of new capacity resulting in commodity DRAM pricing more than doubling during the year," notes Norwood.

SK Hynix and Micron Technology benefited the most from the strong memory market, propelling them both into the top five for the first time. SK Hynix's revenue increased 43.2 percent, the strongest organic growth in the top 25.

The revenue growth was due to its exposure to the booming commodity DRAM market as the industry entered an undersupply and pricing surged. Revenue could have been higher had it not been for a major fire at the company's DRAM fab in Wuxi, China, which accounted for 50 percent of the company's DRAM production.

Micron saw the biggest revenue growth among the top 25 due to its midyear acquisition of Elpida Memory. The company benefited from the recovery in commodity DRAM pricing and strong growth for low-power DRAM where Elpida is strong.

In NAND Flash, Micron was able to aggressively push its NAND into the computing segment, which is projected to represent roughly 60 percent of its demand this year. Had all of Elpida's revenue been included in the Micron number - rather than just the second half - then the U.S. company would have jumped ahead of rival SK Hynix in the rankings.

Vendor Relative Industry Performance

Market share tables by themselves give a good indication of which vendors did well or badly during a year, but they do not tell the whole story. More often than not, a strong or weak performance by a vendor is a result of the overall market growth of the device areas that the vendor participates in.

Gartner's Relative Industry Performance (RIP) index measures the difference between industry-specific growth for a company and actual growth, showing which are transforming their businesses by growing share or moving into new markets.

Market leaders in Gartner's RIP index were MediaTek and Qualcomm, two mobile handset suppliers, which grew 35 percent and 28 percent better than their respective markets. MediaTek accomplished this by focusing on the low- and mid-tier handset segments in China and other emerging markets, a segment of the handset market that is still booming, while Qualcomm dominated the Tier 1 OEMs and high-end segments and wrestled share away from its competitors.

On the other hand, four companies underperformed expectations by more than 10 percent - Rohm, Renesas Electronics, Samsung Electronics and Sony. The three Japanese vendors were hit hard by the rapid devaluation of Japanese currency.

While depreciation of a currency is generally considered as a positive factor for companies to be more competitive when exporting their products, the reality is that the main customers of Japanese semiconductor vendors are typically domestic, and pricing is mostly based in Japanese yen. As the result, yen-based revenue suffers when converted to dollars.

Samsung Electronics maintained the No. 2 position for the 12th year in a row but its overall growth was below the market and its performance in the RIP index was poor.

Three reasons are behind this.

Firstly, Gartner excludes revenue generated from the fabrication of the latest chips for Apple as this is foundry revenue and not merchant sales, so they are captured separately.

Secondly, DRAM revenue growth was less than the market due to Samsung's low exposure to commodity DRAM, which saw a strong price rebound, and the fact that it faced increased competition in low-power DRAM where it is strong.

Finally, the company's own handset business reduced its reliance on the Exynos processor and baseband processor from Samsung's semiconductor operation in favour of competitor Qualcomm.