SEMI: Fab equipment spending to rise by over 20 percent

The uptick to 30 percent depends on specific fab projects in the Europe/Mideast and Asia regions, as detailed in the report.

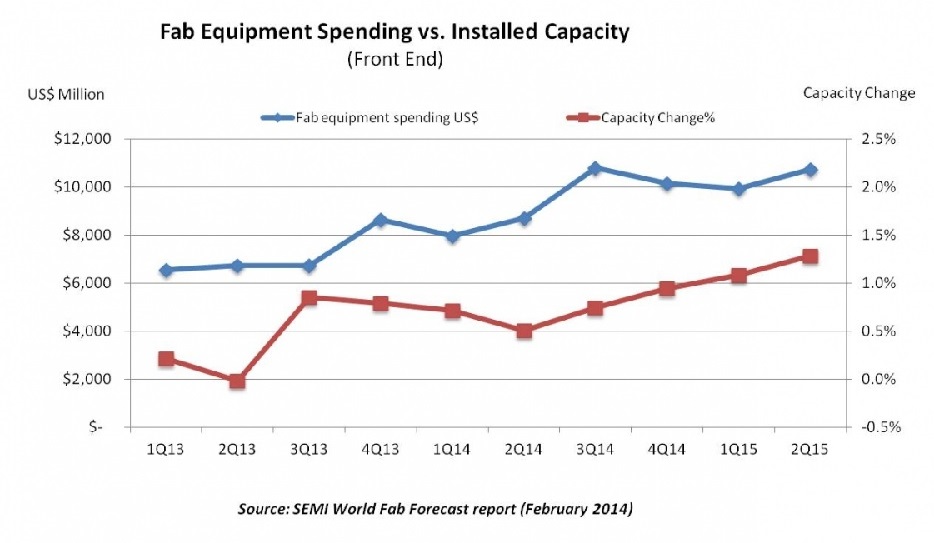

The figure above shows Total Fab Equipment Spending versus Installed Capacity without Discretes.For 2014, the report identified over 190 fab projects in 2014 spending on construction and/or equipment and over such 250 projects in 2015 (including Discretes, LED, Analogue and Logic fabs).

According to the SEMI data, double-digit fab equipment spending growth will occur in almost all industry segments. The segment showing the largest increase is expected to be MPU, followed by Memory. Analogue, Logic and MEMS will share third place with about 30 percent growth each - off of a small spending base in 2013. The Foundry segment spending is expected to grow by 15 percent.

The SEMI report shows an increase in DRAM related projects equipping, thus an increase in DRAM related equipment spending from about 7 percent growth in 2013 to 30 percent in 2014. Overall DRAM installed capacity is expected to remain flat in 2014, following a contraction in 2013.

Equipment spending is also expected to stabilise for both the Opto and the LED fab segments, from 16 percent spending declines in 2013 to 1 percent in 2014. Equipment spending in the LED segment will decline by 9 percent in 2014 following the 21 percent decline in 2013. SEMI estimates construction spending for all Opto/LED facilities will increase by over 60 percent in 2014. These investments will increase installed capacity for LED by 12 percent in 2014 and by about 14 percent in 2015.

Using a bottom up approach, SEMI monitors the installed capacity of more 1,100 facilities. Across the entire industry, installed capacity (without Discretes) grew by only 2 percent in 2013; this is expected to creep up to 3 percent growth in 2014 and in the 3 to 5 percent range in 2015.